— Investment Quotes (@Investor_Quotes) August 30, 2014

Saturday, August 30, 2014

George Soros on upside

— Investment Quotes (@Investor_Quotes) August 30, 2014

Thursday, August 28, 2014

The real things - Laura Ingalls Wilder

“The real things haven’t changed. It is still best to be honest and truthful; to make the most of what we have; to be happy with simple pleasures; and have courage when things go wrong.”

― Laura Ingalls Wilder

― Laura Ingalls Wilder

The Influence Of Charlie Munger

Charlie Munger has had an influence on many an investor. One such person is the respected Michael Mauboussin who counts Munger as a big influence.

He touches on that and other issues in the 36 minute interview below:

https://www.youtube.com/watch?v=6poI6_ds0Po

source: http://www.gurufocus.com/news/267988/36-minutes-of-fun-with-michael-mauboussin--the-influence-of-charlie-munger

He touches on that and other issues in the 36 minute interview below:

https://www.youtube.com/watch?v=6poI6_ds0Po

source: http://www.gurufocus.com/news/267988/36-minutes-of-fun-with-michael-mauboussin--the-influence-of-charlie-munger

3 Reasons IPOs Are Almost Always Bad Investments

3 Reasons IPOs Are Almost Always Bad Investments

Investors are people with a lot of emotions. They get excited by something new, especially if it holds the promise of making them a whole lot richer and provides bragging rights at their next social gathering.

Maybe that’s why amateur and professionals alike tend to lose their minds in bull markets, particularly when a hot initial public offering, or IPO, is offered to them by their broker.

On one hand, had you bought into the IPOs of Infosys, HDFC Bank, Sun Pharma, or TCS, you would have had some volatile price fluctuations along the way, but there is no question that you have made enough money to substantially change the quality of your life. Clearly, a well chosen IPO can be a life changing experience if you simply make the right choice and stick with the stock for years.

On the other hand, there is a large majority of IPOs such as those of Reliance Power, Suzlon and DLF, which have destroyed investors’ capital. With such businesses, even the “long-term” cannot save you from permanent capital destruction.

The Truth about IPOs

Benjamin Graham, the father of value investing, writes in The Intelligent Investor…

In every case, investors have burned themselves on IPOs, have stayed away for at least two years, but have always returned for another scalding. For as long as stock markets have existed, investors have gone through this manic-depressive cycle.

In America’s first great IPO boom back in 1825, a man was said to have been squeezed to death in the stampede of speculators trying to buy shares in the new Bank of Southwark. The wealthiest buyers hired thugs to punch their way to the front of the line. Sure enough, by 1829, stocks had lost roughly 25% of their value.

Over my 11 years of experience in the stock markets, I have rarely come across any IPO that has been launched keeping in mind the interest of investors.

A majority of them have been launched in the form of ‘legalized looting’ by company promoters and their investment bankers.

I have come to believe how Graham defined IPOs in The Intelligent Investor. He said that intelligent investors should conclude that IPO does not stand only for ‘initial public offering’. More accurately, it is a shorthand for…

It’s Probably Overpriced, or

Imaginary Profits Only, or even

Insiders’ Private Opportunity

3 Reasons to Avoid IPOs

There is an old saying in corporate circles. One should raise money when it is available rather than when it is needed. This is the reason most companies come out with their IPOs during rising or bull markets when money is aplenty.

Unfortunately, most investors in these IPOs come out on the losing end of the equation.

Granted, some IPO deals are good for retail investors, but I’d argue the odds of that happening are stacked against you.

The stock market regulator SEBI’s rules that are designed to protect Indian IPO investors, generate reams of disclosures about the company and the offering process but unfortunately, many investors neither read nor understand these.

After all, how many people have the time or inclination to read 400-500 pages of IPO offer documents? And then they say – “Please read the offer document carefully before investing.”

IPOs are not level playing fields, I believe. This game is stacked heavily against the small investor who is lured into the hype and then often loses a large part of his savings betting on listing gains.

Here are 3 reasons I believe small investors must avoid IPOs and rather search for great businesses among those already listed –

1. IPOs are Expensive

People assume an IPO is an opportunity to “get in at lower prices”. In reality, by the time you buy shares of a company in its IPO, other parties have almost always invested earlier at lower prices – often, much lower prices.

Before you even knew about the company, there probably were three or four rounds of private investment, and the per-share price of ownership usually goes up with each round.

In fact, one of the big incentives for an IPO is so that previous investors – founders, venture capital firms, large individual investors – can “cash out” at least a portion of what they’ve invested.

That is why most IPOs are often expensively priced. They are not priced to offer you a piece of the business at cheap or reasonable prices, but to find “bigger fools” who can get in when the “privileged few” are getting out.

Don’t believe the investment bankers when they say that IPOs are “cheap and attractive”. Their incentive lies in first fixing the IPO price (whatever the promoter wants) and then working backwards to justify the same.

2. IPOs Create Vividness Bias

It’s important to understand that the investment bankers and underwriters of IPO are simply salesmen.

The whole IPO process is intentionally hyped up to get as much attention as possible. Since IPOs only happen once for each company, they are often presented as “once in a lifetime” opportunities for the promoters and other large shareholders to cash out.

Promoters and investment bankers thus create stories that are “vivid” – by using terms like “listing gains”, “bright future”, “long-term story” – and entice you to believe them as soon as you hear them.

You must avoid getting charmed by that vividness.

Try to go behind the beauty of that vividness, and scrutinize the IPO to see if it is really so bright and beautiful.

In other words, you need to get past the “bright and shiny” stuff that surrounds IPOs because it’s easy to fall into the trap given that so many others around you are falling for the same.

Don’t buy a stock only because it’s an IPO – do it because it’s a good investment.

3. IPOs Underperform

Most people who get onto the IPO bandwagon often look at the listing or short term gains they can make in the next few weeks and months. In bull markets, this often happens.

However, if you consider the long term performance of IPOs, most of them underperform their peers and the general market – simply because they started off with high valuations.

As you can see in the chart below, the BSE-IPO index has grossly underperformed both the BSE-30 and BSE-200 indices ever since this index was launched in 2004.

Final Word

Investors are people with a lot of emotions. They get excited by something new, especially if it holds the promise of making them a whole lot richer and provides bragging rights at their next social gathering.

Maybe that’s why amateur and professionals alike tend to lose their minds in bull markets, particularly when a hot initial public offering, or IPO, is offered to them by their broker.

On one hand, had you bought into the IPOs of Infosys, HDFC Bank, Sun Pharma, or TCS, you would have had some volatile price fluctuations along the way, but there is no question that you have made enough money to substantially change the quality of your life. Clearly, a well chosen IPO can be a life changing experience if you simply make the right choice and stick with the stock for years.

On the other hand, there is a large majority of IPOs such as those of Reliance Power, Suzlon and DLF, which have destroyed investors’ capital. With such businesses, even the “long-term” cannot save you from permanent capital destruction.

The Truth about IPOs

Benjamin Graham, the father of value investing, writes in The Intelligent Investor…

In every case, investors have burned themselves on IPOs, have stayed away for at least two years, but have always returned for another scalding. For as long as stock markets have existed, investors have gone through this manic-depressive cycle.

In America’s first great IPO boom back in 1825, a man was said to have been squeezed to death in the stampede of speculators trying to buy shares in the new Bank of Southwark. The wealthiest buyers hired thugs to punch their way to the front of the line. Sure enough, by 1829, stocks had lost roughly 25% of their value.

Over my 11 years of experience in the stock markets, I have rarely come across any IPO that has been launched keeping in mind the interest of investors.

A majority of them have been launched in the form of ‘legalized looting’ by company promoters and their investment bankers.

I have come to believe how Graham defined IPOs in The Intelligent Investor. He said that intelligent investors should conclude that IPO does not stand only for ‘initial public offering’. More accurately, it is a shorthand for…

It’s Probably Overpriced, or

Imaginary Profits Only, or even

Insiders’ Private Opportunity

3 Reasons to Avoid IPOs

There is an old saying in corporate circles. One should raise money when it is available rather than when it is needed. This is the reason most companies come out with their IPOs during rising or bull markets when money is aplenty.

Unfortunately, most investors in these IPOs come out on the losing end of the equation.

Granted, some IPO deals are good for retail investors, but I’d argue the odds of that happening are stacked against you.

The stock market regulator SEBI’s rules that are designed to protect Indian IPO investors, generate reams of disclosures about the company and the offering process but unfortunately, many investors neither read nor understand these.

After all, how many people have the time or inclination to read 400-500 pages of IPO offer documents? And then they say – “Please read the offer document carefully before investing.”

IPOs are not level playing fields, I believe. This game is stacked heavily against the small investor who is lured into the hype and then often loses a large part of his savings betting on listing gains.

Here are 3 reasons I believe small investors must avoid IPOs and rather search for great businesses among those already listed –

1. IPOs are Expensive

People assume an IPO is an opportunity to “get in at lower prices”. In reality, by the time you buy shares of a company in its IPO, other parties have almost always invested earlier at lower prices – often, much lower prices.

Before you even knew about the company, there probably were three or four rounds of private investment, and the per-share price of ownership usually goes up with each round.

In fact, one of the big incentives for an IPO is so that previous investors – founders, venture capital firms, large individual investors – can “cash out” at least a portion of what they’ve invested.

That is why most IPOs are often expensively priced. They are not priced to offer you a piece of the business at cheap or reasonable prices, but to find “bigger fools” who can get in when the “privileged few” are getting out.

Don’t believe the investment bankers when they say that IPOs are “cheap and attractive”. Their incentive lies in first fixing the IPO price (whatever the promoter wants) and then working backwards to justify the same.

2. IPOs Create Vividness Bias

It’s important to understand that the investment bankers and underwriters of IPO are simply salesmen.

The whole IPO process is intentionally hyped up to get as much attention as possible. Since IPOs only happen once for each company, they are often presented as “once in a lifetime” opportunities for the promoters and other large shareholders to cash out.

Promoters and investment bankers thus create stories that are “vivid” – by using terms like “listing gains”, “bright future”, “long-term story” – and entice you to believe them as soon as you hear them.

You must avoid getting charmed by that vividness.

Try to go behind the beauty of that vividness, and scrutinize the IPO to see if it is really so bright and beautiful.

In other words, you need to get past the “bright and shiny” stuff that surrounds IPOs because it’s easy to fall into the trap given that so many others around you are falling for the same.

Don’t buy a stock only because it’s an IPO – do it because it’s a good investment.

3. IPOs Underperform

Most people who get onto the IPO bandwagon often look at the listing or short term gains they can make in the next few weeks and months. In bull markets, this often happens.

However, if you consider the long term performance of IPOs, most of them underperform their peers and the general market – simply because they started off with high valuations.

As you can see in the chart below, the BSE-IPO index has grossly underperformed both the BSE-30 and BSE-200 indices ever since this index was launched in 2004.

Final Word

It’s important to remember that, while most are, not every IPO is bad. It’s just that the base rate of investing in an IPO is not in favour of the small investor, and thus you must assess every investment opportunity on its own merit.

Hype and excitement doesn’t necessarily equate to a good investment opportunity.

As Warren Buffett says about IPOs…

Hype and excitement doesn’t necessarily equate to a good investment opportunity.

As Warren Buffett says about IPOs…

It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller (company insiders) to a less-knowledgeable buyer (investors).

If stocks continue to climb this year and the IPO line lengthens, I’m afraid you’ll have plenty of opportunities to see that I’m right.

If stocks continue to climb this year and the IPO line lengthens, I’m afraid you’ll have plenty of opportunities to see that I’m right.

http://www.safalniveshak.com/3-reasons-ipos-are-bad-investments/

source: http://www.safalniveshak.com/3-reasons-ipos-are-bad-investments/

Wealth Wizards: Advice from the Masters

Wealth Wizards: Advice from the Masters

Forbes India: July 11, 2014

S Naren, Chief Investment Officer, ICICI Prudential AMC

Naren's investment philosophy is influenced by US investor Howard Marks's theory that when capital flows are high, it is time to think contrarian. "When you are contrarian and valuations are in your favour - they are the best times to invest in" he says "When you are contrarian, you need to do more research to succeed."

Stay clear of impulse, he insists. " Force yourself to write five lines before you take a decision on why you are buying or selling something," he says. "The main reason why people lose money is because they dont follow a process before taking decisions."

Forbes India: July 11, 2014

S Naren, Chief Investment Officer, ICICI Prudential AMC

Naren's investment philosophy is influenced by US investor Howard Marks's theory that when capital flows are high, it is time to think contrarian. "When you are contrarian and valuations are in your favour - they are the best times to invest in" he says "When you are contrarian, you need to do more research to succeed."

Stay clear of impulse, he insists. " Force yourself to write five lines before you take a decision on why you are buying or selling something," he says. "The main reason why people lose money is because they dont follow a process before taking decisions."

Understand your system

Unless U understand the reason as to why your system makes money, its difficult to distinguish btw temporary setbacks & pernament impariment— Prashanth (@Prashanth_Krish) August 27, 2014

https://twitter.com/Prashanth_Krish/statuses/504652578689269760

Why some of world’s best investors have no finance training

Making students memorize the periodic table but teaching them almost nothing about basic finance is bad enough. But even at the college level, how finance and investing is taught is disconnected from how it actually works. Finance is taught overwhelmingly as a math-based field, in which students learn how to calculate beta by hand and dissect a balance sheet in their sleep. In the real world, finance is overwhelmingly a psychology-based field, where the best investors are those who control their emotions. This is rarely taught and never emphasized. And it's why some of the world's best investors have no formal finance training. Other fields, such as medicine and engineering, have done a much better job preparing students for the real world.-from Fool

From the blog of: Alpha Ideas

Wednesday, August 27, 2014

Shutting down Uber in India was unwise

Shutting down Uber in India was unwise

by Suyash Rai and Ajay Shah.

When you finish a taxi ride, between two to ten minutes are wasted in dealing with the payment. You could pay cash, he might fumble on change, you could swipe a credit card, after an interminable delay the device does not work, and so on.

A few years ago, there was an important innovation in this business by a firm named Uber. Their process flow works like this. The customer goes to the Uber website and submits credit card details (as is done with any E-commerce website). Now he undertakes a ride in a taxi. At the destination, the customer steps out of the taxi and walks away without doing anything on the question of payment. The payment is effected using the pre-stored credit card details. A bill is sent to the customer by email. This saves two to ten minutes for customer(s) and the taxi drivers.

If you multiply millions of taxi rides per year by a saving of two to ten minutes, it adds up to GDP growth. It is estimated that there are 5 million taxi rides per day in India. Assuming that we're dealing with 3 persons per taxi ride, then the new technology will potentially save 91 million man-hours of time for each one minute that is shaved off the payment step. This sort of process innovation is how, one small step at a time, the world achieves productivity growth.

Two days ago, RBI released an order which effectively requires Uber to shut down in India by 31 October.

The problem

RBI has issued multiple regulations imposing specific restrictions on card-based and card-not-present transactions. Instead of a signature, consumers are required to enter a PIN at merchant outlets. For online, card-not-present transactions, we are required to enter one time passwords or other authentication information. Uber was using a loophole in the RBI regulations, which allowed payment transactions with foreign exchange outflow to be exempt from the authentication requirement. The payment was flowing to Uber's bank outside India, and then Uber was sending payment to the taxi driver in India, even though the receipt was issued on behalf of the taxi driver in India. Competing taxi services were also considering such a method of routing payment through a gateway abroad, but it was harder for them to overcome India's capital controls, as they are based in India, unlike Uber which is a foreign company.

RBI's decision creates a level playing field between Uber and Indian taxi companies -- one in which all taxi companies are equally bad in their dealing with consumers, forcing two to ten minutes of time wasted with every ride.

The reason behind this and many other such steps can be found in RBI's overall approach towards regulation. It prefers paternalistic micro-management to market-based solutions.

Need for a composite strategy: prevention and law enforcement

Every month India is clocking about 100 million debit and credit card transactions on Point of Sale (POS) devices, with total value of about Rs.20,000 crore. This means an annual card-based transaction volume of 1.2 billion, with a value of Rs.240,000 crore, and growing fast. Over and above this, there are "card-not-present" or online transactions. In calendar year 2012, the total money lost due to frauds relating to ATMs/Debit Cards/Internet Banking and Credit Card, amounted to about Rs.52 crore. This may seem like a very small number compared to the total value of payments, but each instance of fraud is a crime and must be dealt with. This raises questions about consumer protection and law enforcement.

The consumer protection objective in this context is: consumers' funds must be protected from fraud. The question is: how should this be done? There are basically two approaches to this: prevention and enforcement. Both are important in an overall anti-fraud strategy. The regulator can impose security requirements that make it difficult to defraud customers, but each requirement has costs. Law enforcement can also help the consumer recover the money lost to fraud, but this also has costs and the consumers may get their money with a time lag or not at all.

When it comes to prevention, it is important to consider who is best placed to develop and implement preventive steps. This responsibility can be substantially shared by service providers, who are often better placed to make the right preventive choices, as long as they are held accountable. Service providers, in any case, have an interest in maintaining trust in their systems, and in addition to that, they could be held accountable by the regulator.

What has India's approach been?

RBI has been writing `regulations' to address this problem which have largely been paternalistic, micro-managing, and technology-specific. Earlier, one could make a card-based transaction by simply swiping a card and signing on the slip, but now one must enter PIN in the POS device. This has made every transaction more cumbersome, especially where the POS device is not present in the immediate vicinity of the transaction (e.g. at restaurants). Earlier, one could transact online (called "card not present" transactions), with one factor of authentication, but now two factors are required, one of which is often a one-time password, generated and sent over the mobile network or on email. Given the relatively low reliability of SMS in India, this often leads to delays and failed transactions. In the world of E-commerce, all over the world, customers link a credit card to a merchant website once, and transact at wish. This is not allowed in India. In addition, RBI has imposed several requirements on technological specifications for cards, POS devices, etc.

These measures have improved security of transactions. But were they optimal? Do they pass the test of cost-benefit analysis? Effectiveness of a measure is not the only consideration. Excessive regulation can be effective but not efficient. Regulators such as RBI have enormous powers, and they must always be asked to defend the use of these powers - on effectiveness, efficiency, and jurisdiction. This is essential to ensure accountability of these agencies.

All preventive measures impose costs on consumers, and, on the margins, create a preference for cash payments and contribute to the tendency to avoid online transactions and the white economy. On the other hand, they also increase robustness of transactions, thus increasing the trust in these systems, and encouraging greater participation in these systems. When we look closely we find that all payment transactions do not pose the same level of security risk. Systems can enable small-value transactions with minimal friction, and require significant authentication processes for higher value transactions. Some transactions might justify 3 factors of authentication, but some other transactions may require just 1 factor. Regulatory intervention at system level takes a one-size-fit-all approach, which is costly. So, preventive measures are crucial, but they need to be proportionate to risks. This proportionality cannot be achieved by regulatory diktat. It must come from innovative market practices. The incentive for such innovation is destroyed by RBI's paternalistic approach. The counter-factual world that we do not see is one where innovative firms in the business of payments invent improved methods of risk management.

What about law enforcement?

Payment fraud is a crime, and it should be looked at from that lens. When it comes to crime, it is often easy to prevent it by imposing excessive restrictions on potential victims. It would be easier to prevent pickpocketing, if people are mandated to carry wallets attached with chains to their clothes. Does that mean we should mandate such costs to be incurred by the people? Most would laugh at the very suggestion. And yet, for crime prevention in electronic payments, we easily accept the entire country to spend a few extra minutes on every transaction, or to give up the enormous convenience of automatic transactions on linked cards.

Public choice theory teaches us that bureaucrats and politicians are self-interested actors, and work for themselves -- not for the people of India.It is always convenient for government agencies to ratchet up prevention because they then have to do less work on enforcement. As citizens, we must push back against such behaviour. Better enforcement generates deterrence and is hence an important tool for prevention. But it requires more work on the government, and all too often government agencies prefer the laziness of shutting down activities.

How to do better

The government must not hinder innovation in business models and technology. As Percy Mistry says: Elsewhere in the world, the government fits the needs of the economy, but in India, the economy is forced to fit the needs of the government. This must be turned upside down. In the long run, nothing matters as much to India as achieving higher productivity, which requires that organisations such as RBI need to stop blocking progress. The right attitude at RBI should have been: "Uber has come up with an interesting innovation, how do modify our rules and procedures so that everyone in India can utilise such innovative business models?".

The foundation of the regulatory strategy should be principles of responsibility: who will be held responsible under what circumstances. If the consumers has been excessively lax, then he should take responsibility for the failure, and if the payment service provider has not implemented adequate security measures, then it should be held accountable. Once Uber or Paypal know they are responsible, they have the best incentive to innovate on technologies of security. Clarity on consumer protection, as is done in the draft Indian Financial Code, should shape these principles of responsibility. This is the business of financial regulation.

Employees of the government almost always do not know enough to interfere in technology. `How to produce' should be the exclusive preserve of the private sector. See Hrush Bhatt of Cleartrip responding to RBI's rules about two factor authentication.

The regulator should define a proportionality principle for security of payment transactions, and then leave it to the payment service providers to choose and implement risk-based security approaches. This will lead to innovation in payment security. For example, a payment service provider may choose to implement a minimal authentication process for low value transactions. Or, they could link it to the credit limit or available balance, so that the poor consumers are disproportionately protected.

Enforcement is hard work, and prevention is easy by shutting down complexity in the economy. Regulators must almost always avoid banning things, and work harder on developing State capacity in enforcement. In many instances, neither the consumer nor the provider would be responsible, and it would be a crime that could not have been reasonably prevented. In such instances, enforcement is the only option.

Two laws gave RBI the raw material to shut down Uber: the Foreign Exchange Management Act (which gives power to hamper all cross-border transactions) and the Payment and Settlement Systems Act (which gives power to hamper innovation in payments). These laws are incompatible with progress, as has been argued by the Financial Sector Legislative Reforms Commission (FSLRC).

The regulator should supply the public goods of data and foster research on payments and security and the performance of alternative authentication mechanisms.

The most important ingredient required for progress is humility. These are complex problems. The simplistic, overly prescriptive and paternalistic approach is harmful. In India, the costs of such an approach could keep people away from the financial system. The use of cash is even riskier than a relatively less secure electronic payment system. Cash is friendlier to money laundering, terrorism financing and fraud. That is the continuum of choices. A costly, one-size-fit-all, prescriptive approach may lead to high security for those in the electronic payment system, but may be leaving a large number of people out.

What Phil Libin, the CEO of Evernote, says about decision making in corporations is equally true of the world of public policy:

"We always try to ask whether a particular policy exists because it’s a default piece of corporate stupidity that everyone expects you to have, or does it actually help you accomplish something? And very often you realise that you don’t really know why you’re doing it this way, so we just stop doing it."

How to make RBI serve the needs of India?

RBI's intervention is problematic from a legal process perspective. Regulators are mini-states with legislative, executive and judicial powers. Such powers are easily misused, especially in name of doing good. Payments is just one area where productivity-enhancing innovations are being hampered in the name of security. In fact, many bad things are done with some noble objective serving as justification. Bad behaviour need not mean stereotypical corrupt behaviour. It could also mean other things, such as taking excessively restrictive steps, because the regulator wants to make its life easy. For example, giving two bank licenses per decade, just to reduce the amount of work required in supervision, is also bad behaviour. So, we must be a little more circumspect with agencies like RBI. They need to be held accountable. One good way of ensuring good behaviour is to mandate them to follow certain process of making and enforcing regulations.

The principle of proportionality, market-based innovations on security, and strong enforcement, are the magic ingredients for achieving optimal security in payment. Only careful analysis, and continuous review can reveal the right mix. Cost-benefit analysis of regulations will help choose the most efficient regulatory pathway to an objective. This analysis requires the regulator to list a few plausible regulatory alternatives, compute their costs and benefits for the entire economy, and choose the most efficient alternative. In case of payment security, at least two types of stylised choices are possible: those making specific prescriptions that payment services providers must follow, and those holding the service providers accountable for ensuring proportional security. Analysis would reveal which approach would work in what context. The world is changing rapidly, and the regulator must keep on learning. Hence, each such regulation must be subjected to periodic reviews, to understand what effect it had on the economy, and to make course corrections.

Such cost-benefit analysis and ex-post review are parts of the regulation making process in many good countries. They have also been recommended in the draft Indian Financial Code formulated by the Financial Sector Legislative Reforms Commission (FSLRC). Indeed, decades of observation of the blunders of financial agencies in India, of the sort being discussed here, is what has given the subtleties of the draft Indian Financial Code. You may like to see this talk on how to obtain progress on payments.

Source: http://ajayshahblog.blogspot.in/2014/08/shutting-down-uber-in-india-was-unwise.html

A Snowman in the Summer Sun

Summary:

- SLL is a leader in cold chain infra and logistics, has synergies with promoter Gateway Distriparks

- It’s a high demand sector, with good growth prospects, visible food wastage and govt. support.

- Seen rapid growth from small base – Income, EBITDA, Profits have grown 43, 51 and 55% CAGR

- The market is looking positive and open to such offerings.

- Risks include aggressive opportunistic IPO pricing and negative cash flows.

- Advice: Buy with a medium term, 1 year perspective

Introduction

- Snowman Logistics is a Bangalore based firm with a cold chain and distribution network.

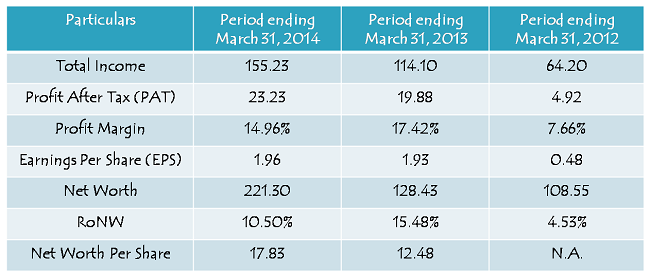

- It operates 23 temperature controlled warehouses (at 14 locations) and 370 reefer transport vehicles.

- Revenues in FY14 were Rs 155 cr and Profits 23 cr. It has 1490 employees (but only 383 permanent).

- Started 21 years ago as Snowman Frozen Foods, and attracted investors like HUL and Gateway Distriparks.

- The leadership team is Gopinath Pillai – Chairman and Kannan Ravindran Naidu – Director & CEO.

- Key customers are Baskin Robbins, McCain Foods, HUL, Fererro India and Novozymes South Asia.

- SLL is now a subsidiary of Gateway Distriparks Ltd (GDL), an integrated logistics firm of market cap of 2,800 cr. The firm has been a good performer for investors over the last 6 years.

- Business segments are split across warehousing and distribution, see revenue segments in Fig 1a.

Fig 1a – Revenue Breakdown and Fig 1b – Shareholding post IPO (click on image to enlarge)

IPO Highlights

- In this IPO there are 4.2 cr. shares of Face Value 10 each, which make up 25.2% of equity post IPO issue.

- Retail investor quota is only 10% of the issue, 15% is reserved for non-institutional investors while the balance 75% is available for qualified institutional buyers. See Fig 1b for post IPO pattern.

- The Price range: Rs. 44 – 47, and the amount range to be raised: Rs. 185 – 197 cr. will be used for:

- Capital expenditure for new temperature controlled / ambient warehouses of 128.3 cr.

- Long term working capital of 8.4 cr. Rest of funds will be utilized for general corporate purposes.

- The P/E of SLL is 31.5 – 33.7 times at Lower – Upper price limits, based on the FY14 nos.

- Post IPO, the market cap of the firm will be 783 cr. (upper end).

- News – SLL has decided to allot 44.4 cr worth of shares (94.5 lakh shares at higher end of Rs 47) to three anchor investors, Faering Capital India Evolving Fund, ICICI Prudential and IDFC Funds.

- The Issue has been graded by CRISIL Ltd as 4/5, indicating that the fundamentals of the Issue are above average in relation to other listed equity securities in India.

Snapshot of promoter firm Gateway Distriparks

Since GDL is the holding company and Promoter of SLL, we will do a quick analysis of this firm.

- GDL is a logistics player with 3 verticals – Container Freight Stations (CFS), Inland Container Depots (ICD) with rail movement of containers to maritime ports, and Cold Chain Storage and Logistics – SLL.

- It had a 2005 IPO at Rs 72. The share had a fair performance, appreciating at average 13.6% annually over 9 years, from the IPO level. Much of these gains came in the last 1 year when it shot up from 100.5 to CMP. However including a (2007) bonus and regular dividends, gains are 21% annually.

- The Income, EBITDA and Profits have grown at 24.7%, 15.1% and 12.5% CAGR over the last 7 years.

- The Blackstone Group made a private equity investment in 2009 in the GDL subsidiary, Gateway Rail.

- The promoter group hold 38% of GDL, of which 49% (18.7% overall) is pledged. This is a negative.

- GDL standalone has good cash flow, as the firm has been FCF positive over 5 years.

- Investors have been fairly rewarded for their shareholding in this firm.

- Today GDL is available at a P/E valuation of 19.6 times. See Fig 2.

- This is a background/indicator for performance of the IPO of subsidiary SLL from same promoters.

Fig 2 – GDL Financials Snapshot (click on image to enlarge)

Financials of Snowman Logistics

- The Income, EBITDA, Profits & EPS have grown 43.2, 50.5, 54.8 and 54.7% CAGR over last 5 years.

- The margins are fair with Operating and Profit margins at 26% and 15% for FY14. Fig 3.

- Top 20 customers contributed 44.1% of revenues (2014) indicating good customer diversification.

- The D/E of the firm post IPO will be 0.54. This is a good ratio, particularly for this industry.

- Price to Book Value is at 3.5 for FY14, a little expensive.

- RoCE and RoE metrics are at 6.5 and 10.1 in FY14, which are fair.

Fig 3 – Financials, Source: Company data (click on image to enlarge)

- The business has been Cash Flow negative for the last 5 years. See Fig 4.

Fig 4 – Cash Flow of SLL

Business and Industry Notes and Trends

- SLL’s expansion plan involves the set-up of warehouses, six temperature controlled and two ambient, in six cities. The pallet capacity should increase from 61,543 pallets (FY14) to 85,000 pallets (FY15) and to 100,000 pallets (FY16). This is likely to boost the operations of SLL over 3 years. (Pallet is a unit of load which allows for efficient handling and storage of products in warehouses).

- The customer segments include Dairy Products – Milk, Butter, Cheese, Fruits & veg, pulp, canned food, Meat & Poultry, Beef, Seafood, pharmaceuticals and Packaged consumer Products.

- Industry Notes: The logistics business requires a large initial capital investment in land, warehouse, and equipment and then client acquisition and operations, which finally results in capacity utilization and revenue. Thus revenues increase only 2-3 years after investment starts. The business is very investment and cash flow intensive, with a mid to high gestation period. The challenge in logistics is also to achieve critical mass, operations scale, capacity utilization and minimum business volumes.

- Demand drivers: India’s per capita income has grown at a five-year CAGR of 16%. Food has grown in terms of absolute consumption. In addition to fruits and vegetables (F&V), the value added foods, Quick Service Restaurants, ice cream chains and packaged foods segments have grown rapidly.

- The temperature controlled logistics industry in India is estimated at nearly 15,000 crore and expected to grow at 15-20% in the next 3-4 years. Further, the industry remains fragmented and unorganised and only 6-7% comes in the organised sector.

- Massive wastages in transportation of F&V, can be addressed by an upgradation of the cold chain.

- Trends: A long term trend is of logistics services moving from unorganized to organized sector. This may accelerate given the brand, support and guarantees that can be offered by larger players.

- Another trend is towards specialization and outsourcing of logistic processes to vendors like SLL. Modern firms stay lean by focusing on core competences and partnering to stay efficient.

Positives for Snowman Logistics in the IPO

- Rating agency CRISIL has rated its IPO at 4/5. This is an excellent rating.

- The demand from food, pharma and consumer product industries likely to grow steadily. Proliferation of multinational QSR chains should also help pan-India cold chain logistics players.

- Value added services can be a high potential segment that can boost profits for SLL.

- The equity investment climate has improved in the last 6 months. Logistics firms have seen their valuation improve, and the sector outlook has improved based on anticipated economic revival.

- SLL is a leader in the cold chain logistics sector, far ahead of other organized sector players. With pan-India operations and growth plan, SLL may be able to achieve the critical mass and business volumes required to sustain investments and operations and generate high profits.

- SLL has a 21 year history of cold chain services and has built expertise in this area. It has experienced promoters and leadership that manage the operations of the company.

- From a small base, SLL financials have grown at very good rates of 43-54% CAGR over 5 years.

- Good parentage, with GDL having sustained and survived the tough economic climate of 2007-14. GDL may do much better in the next few years. This expertise should certainly rub off on SLL. Synergies with GDL include common customers, good GDL network and similar systems / processes.

- Serving diverse end-products helps SLL to counter demand volatility as the end-products that require cold storage have seasonal demand. This helps run facilities at high utilization all year long.

- Tax benefits available to SLL under Section 35 AD will help the company. The sector has infra status.

Risks and Challenges

- Stretched valuations: At a P/E range of 31.5 – 33.7 times trailing twelve months earnings, the price ask is surely high. Even parent GDL is available at 19.6 times, much more reasonable.

- A smaller portion (than most IPOs) is available for Retail, indicating that issuers are targeting investments from deep pocketed institutions. This may crowd out retail from IPO allotments.

- The trio of labor, fuel and power form a large chunk of expenses of SLL, and these have been rising rapidly in the last few quarters due to external events.

- A slowdown in economic growth in India could cause the business at SLL to suffer.

- Competition from existing and new players. Cold Chain operations are embedded in the business of firms like Concor and Gati. The unorganized sector is large and competes on price.

- While pledging of shares by GDL (to raise funds) is seen in many infra players, it is a systemically risky practice and a sign of poor free cash flows, long gestation projects, or both. A sudden share price fall due to any factor can result in an unwinding by the brokers, triggering a further price fall.

- The cash flow history of SLL is poor and it is still bleeding cash. In addition there is a stated IPO objective to invest in further expansions. Cash flow positive status is at least 2-3 years away.

- If expansion plans are not implemented in a timely and efficient manner due to any reasons, it could adversely affect the business performance. Typically land permits and local permissions are important here and are notoriously unpredictable to obtain.

- So far, funding for growth of SLL has come partially from Private equity and VC players. Post listing, SLL will have to use the IPO proceeds for investments and thereafter be able to fund its growth out of internal cash generation. This is an inevitable challenge at this stage of business growth.

- The GDL group is financially controlled by the Delhi-based businessman, Prem Kishan Gupta, whose connection with a 1998-CBI case casts a shadow on the Gateway group image.

Benchmarking

We will benchmark SLL against peer logistics listed firms.

Fig 5 – Benchmarking

Based on the benchmarking chart Fig 5, we have the following thoughts

- The high growth of SLL matches with high valuation parameters like P/E and P/B.

- Margins are on the higher side, which is good

- RoE is high, but RoCE is low among peers indicating an investment phase in logistics operations.

Overall Opinion

- There’s no doubt that Snowman is a leader in its niche of cold chain logistics. It is also a high demand sector where (assuming fair services pricing) capacities created will be quickly utilized.

- The pricing of this IPO is high and opportunistic, and assumes high growth rates will continue. It is high even compared to the parent GDL, and peers in the sector. Hence we have – A Snowman in the Summer Sun.

- This sector has cash flow challenges, and needs long investment cycles. Investors will realize that very few corporates from infra sector are good long term investments compared with other sectors.

- Having said all this, this is a good investment climate for the logistics sector. The market is overall positive these days post budget, and this small cap IPO is likely to sail through easily.

- There may also be a good pop on listing as the 3 day IPO is already subscribed 83% on Day 1. Retail has dominated so far, and this category has already been subscribed 270% of the quota. Track further on LINK.

- Based on all this, the SLL IPO is a buy with a medium term, 1 year perspective.

Source: http://jainmatrix.com/2014/08/27/snowman-logistics-ipo/

The Scientific 7-Minute Workout

Source: http://well.blogs.nytimes.com/2013/05/09/the-scientific-7-minute-workout/?_php=true&_type=blogs&_php=true&_type=blogs&smid=tw-share&_r=1&

Lessons In Non-Profit Storytelling From The Best In The World

If you think times are tough in a marketing world where you’re actually providing goods or services in exchange for money, spare a thought for the marketers of charities who need to convince us to part with money without wrapping up something for us to take home.

One of the biggest challenges non-profits face is justifying their operating costs. Supporters of charities have long questioned the amount of money spent on admin vs. how much actually creates impact for the worthy cause they donated to.

The Internet has made it easier for charities to reach people and to tell their story, but that access has also created a new breed of supporter who is both savvy and discerning. Access shouldn’t be confused with impact though. There are no shortcuts to mattering to people, but there are ways you can tell a better brand story.

7 Lessons In Non-Profit Marketing From charity: water

1. Declare a single enemy.

charity: water’s is dirty water. They explain how lack of access to clean drinking water impacts everything from health to time, poverty to education and the effect on the lives of women and children in particular.

2. The 100% giving model.

Build trust with transparency. charity: water stripped away all doubt about how much of the donated funds actually impacted good causes. They have two funding streams, donations to water projects from supporters and private donors and sponsors who fund operating costs. Donations are tracked to results in the field using photos and GPS so that supporters can see their impact.

3. Provide context

The size of the problem is still big (a billion people don’t have access to clean water), but charity: water breaks it down. They make the real impact of the donation more tangible.

My $20 buys access to clean water for one person.

4. Understand the donor’s worldview.

charity: water knows that we were buying the feeling that giving brings.

They worked out what supporters needed to know and how they wanted to feel and used great storytellingto make that happen.

5. Make it personal

The my charity: water platform gives people the opportunity to create their own campaign and a way to reach out to and connect with their supporters. This platform also makes it easy to both fundraisers and supporters to donate, keep track of progress and feel involved.

There are regular campaigns encouraging people to ‘donate’ their celebrations, like birthdays to the cause.

6. Leverage design.

Take a look at the charity: water website and you’ll see what I mean. Many charity websites feel clunky, they often have the feel of a dated corporate bureaucracy. This one feels like it’s alive, that it’s powered by community and intention, that work being done. The charity also has a recognisable symbol— the yellow jerry can.

7. Create community

charity: water makes it easy to share their story and your campaign via social media. They leverage all of the modern brand storytelling tools to both share the joy and create a sense of community.

Here is the charity: water Difference Map (created by me for the book Difference, not in consultation with charity: water). It might give you some clues about how to tell your own story.

Source: http://thestoryoftelling.us2.list-manage1.com/track/click?u=9098bcad3babe863ca266c364&id=6259fd970a&e=5f961d9eca

Personally, i love everything Bernadette Jiwa writes. Big fan of the story of telling

The stock market is terribly misunderstood

The stock market is terribly misunderstood - Subramoney

Caveat: I like equity markets, as a family my father started investing in 1950s, I started investing in 1979, have enjoyed the process so far. I am completely indifferent to YOUR views on the market and whether you invest, hate, love or are obsessed with the market.

Article: The equity markets are one of the most misunderstood markets and you have people with very strong views.

Let us examine them: 1. You can make a lot of money in the equity markets: Even for big brilliant investors like a Warren Buffet or a Vallabh Bhansali, remember it is a few right calls, and YEARS OF SITTING on good calls. It is the power of compounding that has worked. In case of WB about 99% of his wealth was created AFTER his age of 50 years. Remember he started at age 11?

2. If you had invested in 1994 till the year 2014 you earned LESS than PPF: Only an absolutely idiotic person can write such an article. One needs to remember that even the index scrips would have paid about 3% annual dividend. Now if this dividend was REINVESTED in the same index, the returns would go up to about 7-8% over a 20 year period. ET’s Innumeracy.

3. Some people argue ‘What if I had invested in Satyam or Silverline instead of Infy or Wipro?: Look you genius, if you do not know how to pick stocks stick to mutual funds. If you know how to pick stocks, be vigilant. Stock picking is not Rocket Science – like riding a cycle – but it has to be learnt. People like Pattabhiraman (of Freefincal.com) can learn, but obviously lacks time. To learn about markets you need time and intellect. Having one cannot be substituted by the other.

4. Taking a view of the market is not my cup of tea I do not understand interest rates, technical analysis, fundamental analysis, etc. And I find it difficult to watch TV on a 24 hour basis: Well the good news is YOU need not know why somebody is raving and ranting about the Chinese economy, US slow down, Indian election, etc. Even assuming that all this is very important, if you pick a good company with a good business model, and have a long term view, the short term machinations of the market should not bother you. Just keep the media out of your investing life.

5. My father lost money in Harshad Mehta scam, CRB scam, Ketan…..Look it is not as if these people came to your father and asked him to invest. He chose to invest in companies that he did not understand, with the help of people who said money could be made. Be dispassionate in the analysis, stop blaming the markets. Do you stop sleeping on a cot because your grandfather died while sleeping on a cot?

6. There are short cuts in the market: I have not found them. It takes time to build contacts, understand markets, understand many things from Anthropology, Aviation, Ethics, Biology, Geography, Psychology, Philosophy, Accountancy, Human Behavior, Mathematics, Statistics, Equity Research….it also helps if you know some top Accountants, Lawyers, Research guys, Brokers, Fund managers, Fund analysts, Fund sales guys, etc. If you think you could read a couple of websites and make tons of money, revisit your thoughts.

7. WB’s techniques will work for me! Sure, when you reach the size of WB. Stop believing you can invest like WB or Mukesh Ambani. You cannot. Somethings can be achieved ONLY by size. If I buy 2000 Tata Power and 3000 Coromandel International – I should not confuse my self with a Rakesh who buys 500,000 in one shot, and can buy another 200,000 after a week. Or like another friend who bought 2 million shares in a company where I have under 40k shares. Size matters. Research matters too.

Source: http://www.subramoney.com/2014/08/the-stock-market-is-terribly-misunderstood/#sthash.a12kyifK.dpuf

Cant agree more with the article! Love point number 5, 6 and 7

Snowman Logistics IPO Review

Gateway Distriparks’ 54.04% owned subsidiary, Snowman Logistics Limited, is coming out with its initial public offer (IPO) from tomorrow i.e. August 26. The company has floated the issue with a price band between Rs. 44-47 per share and is offering 4.20 crore shares during the offer period. The offer will remain open for three days to close on August 28.

At Rs. 47 per share, the company plans to raise Rs. 197.40 crore in the IPO. The face value of its shares is Rs. 10 and thus, the issue commands a premium of Rs. 34-37 to its face value. As the company’s average pre-tax profits in 3 of the preceding 5 years was less than Rs. 15 crore, only 10% of the issue size is reserved for the retail individual investors.

About Snowman and its Operations

Gateway Distriparks owns majority of Snowman Logistics outstanding shares as its shareholding stands at 54.04%. Snowman’s other large shareholders include Norwest Venture Partners VII-A Mauritius (13.78%), Mitsubishi Corporation (12.57%), International Finance Corporation (12.40%), Mitsubishi Logistics Corporation (2.92%) and Laguna International Pte. Ltd. (1.57%).

Snowman is engaged in offering integrated temperature controlled logistics (TCL) services including warehousing and distribution of frozen and chilled products like dairy products including butter and cheese, ice-cream, poultry and meat, seafood, ready-to-eat/ready-to-cook food products, confectioneries including chocolates and baked products, fruits and vegetables, healthcare and pharmaceutical products and industrial products such as x-ray and photo imaging films.

As of March 31, 2014, Snowman carried out its operations having 23 temperature controlled warehouses across 14 locations in India including Serampore (near Kolkata), Taloja (near Mumbai), Palwal (near Delhi), Mevalurkuppam, (near Chennai) and Bengaluru capable of warehousing 58,543 pallets and 3,000 ambient pallets. Further, it had 370 Reefer vehicles consisting of 307 leased and 63 owned vehicles with a total workforce of 1,490 including 383 permanent employees and 1,107 on a contract labour basis.

Snowman has a diversified customer base with top 20 customers contributing approximately 44.10% of its total revenues during FY 2013-14. Its top 20 customers include Hindustan Unilever Limited (HUL), Al-Karim Exports Private Limited, McCain Foods India Pvt. Ltd., Novozyme South Asia Pvt. Ltd., Ferrero India Pvt. Ltd. and Graviss Foods Private Limited.

Objectives of the Issue - Out of Rs. 197.40 crore it targets to raise in this issue, Snowman plans to use approximately Rs. 128.28 crore to set up 6 temperature controlled warehouses and 2 ambient warehouses in various cities including Taloja (near Mumbai), Cuttack, Pune, Mevalurkuppam (near Chennai), Visakhapatnam, Pune and Surat.

IPO Grading - The issue has been graded by CRISIL as 4 out of 5, indicating that the issue is fundamentally above average relative to other listed equity securities. However, this grading is neither a recommendation to subscribe or not to subscribe to the issue nor an opinion of CRISIL whether the issue price is appropriate in relation to the fundamentals of the company.

Minimum/Maximum Subscription - Market lot of the issue is 300 shares and thus the investors would be required to bid for at least 300 equity shares in the IPO i.e. a minimum investment of Rs. 14,100. Retail investors would be able to apply for a maximum of 4,200 shares at the ‘Cut-Off’ price.

Listing - The company will get its shares listed for trading on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) within 12 working days from the closing date of the issue.

Risks

* The company is yet to obtain certain approvals/licenses for warehouses for which the funds are being raised through the issue.

* Profitability of the company is quite sensitive to power and fuel costs. Any significant increase in these costs or any continuous or chronic interruption in power supply to the warehousing facilities will have a material adverse impact on its operations.

* The company operates 307 of its 370 reefer vehicles and 13 of its 23 temperature controlled warehouses on lease. For these operations to run smoothly, the company is dependent on third party service providers. Any disruption in operations due to any unforeseen reason might result in below par operating performance.

Financials of the Company

(Figures are in Rs. Crore, except per share data & percentage figures)

Anchor Investment - Three Anchor Investors, IDFC, ICICI Prudential and Faering Capital, have been allotted 94.50 lakh shares of the company today at Rs. 47 i.e. the upper end of the price band. IDFC has been allotted approximately 26.6 lakh shares for IDFC Sterling Equity Fund and 3.19 lakh shares for IDFC Infrastructure Fund, whereas ICICI Prudential has been allotted 21.28 lakh shares for ICICI Prudential Growth Fund – Series 2 and 8.51 lakh shares for ICICI Prudential Value Fund – Series 4.

Valuations

Snowman reported a growth of 16.85% in its profit after tax during the last financial year. Assuming a similar growth this financial year as well, the price band of Rs. 44-47 values the company at around 27 times to 29 times on an expanded equity base post-IPO. Considering a short to medium term operating history, these valuations seem to be on a higher side to me.

But, at the same time, considering the cold storage to be a sunrise industry with infrastructure status tag, there is an immense potential of growth and thus, the issue looks attractive with a little risk involved. Though the issue looks attractive from the listing gains perspective, I think the investors should invest in this issue from a long-term perspective. If things pan out well, I expect the issue to generate good returns for the investors over a period of 2-3 years.

Investors would do well to keep a close eye on the company’s operating performance on a regular basis. Any significant deviation from its expected operating performance should be analysed thoroughly.

http://www.onemint.com/2014/08/25/snowman-logistics-ipo-review/

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Tuesday, August 26, 2014

Dan Coats

Every time i recite this in my head, i remember you prof Maya Baltazar Herrera

“Character cannot be summoned at the moment of crisis if it has been squandered by years of compromise and rationalization. The only testing ground for the heroic is the mundane. The only preparation for that one profound decision which can change a life, or even a nation, is those hundreds of half-conscious, self-defining, seemingly insignificant decisions made in private. Habit is the daily battleground of character.” - Dan Coats

“Character cannot be summoned at the moment of crisis if it has been squandered by years of compromise and rationalization. The only testing ground for the heroic is the mundane. The only preparation for that one profound decision which can change a life, or even a nation, is those hundreds of half-conscious, self-defining, seemingly insignificant decisions made in private. Habit is the daily battleground of character.” - Dan Coats

Repost: Fluidomat Ltd

From:

Arun the Stock Guru -Stocks,Tr

Stock tip:-

Scripscan:Fluidomat Ltd

Bse code:522017

Cmp:131rs

Target:195rs

Return percentage:50%

Duration:9-12 months

Quote:It was very difficult to dig about this company as management always been very very reluctant to speak.Thanks to my analyst buddies Keshav and Saurav for their inputs and research notes which helped me in getting aware of the most about the company.

Business:Fluidomat Ltd. makes Fluid Couplings.Google up to know what a fluid coupling is all about.Fluid Coupling is a Power Transmission Product.It is a Capital Good & not a consumable.Fluidomat has supplied more than 900 Scoop Control Couplings and several thousand constant fill fluid couplings on variety of applications in all sectors of industry including Coal base Power Plants, Steel, Cement, Paper, Chemical & fertilizer industry, Petrochemical Industry,Underground & Open Pit Coal and Mines, Harbor Handling and Nuclear Power Generation Plants in India and Abroad.Around 75% of the Revenues of the company are from the Power Sector.Sales growth of the company is dependent upon the Capex in these industries.

Market Size:Around 230crs in India and several times more internationally.Huge export potential for the company.Main thrust is on the Domestic Market, though the co. has expectations in Australia, Indonesia, Malaysia & Brazil(from the mining sector). The company has appointed dealers in these geographies.

Clients:ABB, BHEL, Braithwaite, Burn Standard, CIMMCO, Chemical Construction, DEMACH, DCIPS, ELECON, EPIL, FFE, Fuller KCP, Flakt, Flender, HEC, HDOL, HSML, INDURE, Krupp, Kirloskar, Kraft Engg., L&T, MAMC, MBE, Metso, MECON, Naveen, Oilex, Penwalt, Promac, Reitz, Sayaji Iron, Techpro,Thermax, TLT, TRF, Walchandnagar Industries, Warman etc.

Approvals from the Consultants:Fluidomat Fluid Couplings are approved by all leading industries and consultants in the country. The consultants include ACC, BHEL, Birla Tech Services, DCPL, Desin, HOWE India, Holtech, Jacobs, MECON, MN Dastur, NTPC, Tata Consultants,Tata Projects, Samsung, Doosan (Korea), Hyundai (Korea), Alstom (France), Sulzer (Germany) etc.Its also got a tie up with flow serve (Spanish company).They too have requirement for these couplings.

Price Range of company products = Rs.12,000/- to Rs.80 lakhs.

Competitors:Premium Energy Transmission Ltd., Elecon Engg. Ltd. & Voith (German). Apart from Voith,all others have rented tech.Main competition is from voith but with time I feel fluidomat would be able to beat voith comfortably.Voith’s pricing is 3 to 10X of fluidomat for same products.

Service cycle:FCs can last for 25-30 years also,typical replacement cycle is 10-12 years.In government departments specific budgets are allocated,hence they tend to replace their couplings earlier at 5-6 years as if these budgets are not used they are extinguished.

Points to look for:-

1)There is no unorganised sector in Fluid Couplings due to the hitech nature of the product.Also Fluid Couplings are very crucial products and reliably is a big factor. If it fails then the whole plant comes to a standstill.

2)The company does not require much capex.Land and building are excess.It can grow to Rs80-100 Cr turnover by adding only CNC machines.Capex could 1-2 Cr per annum.The company has started manufacturing FCs for fans used in boilers. It is now supplying the same to BHEL. Voith is the only competitor in this segment. The company entered into this segment three years ago based on indigenious R&D.

3)Fluidomat has also concluded designs for less than 110 MW boilers.It will enter this market soon.Working capital requirement for company's business is 3-4 months.Cycle is long as until the entire order is ready inspections don’t start(Debtor Days thus being 100).The company does not face issues on account of bad debtors as it supplies very critical equipment.

4)The company has started supplying FCs to NTPC also in the last year.Here again voith was the competition.Voith used to charge 4 Cr for one coupling which the company is supplying for 45 lakhs.In Jan 15 these couplings would complete one year of functioning.If the operation is glitch free.The company will be automatically approved for all future orders of NTPC.

5)The company is vertically integrated.It has its own foundry and fabrication facilities.The company has got cash and bank balance of 10crs as on date.Thats more than 20rs per share.Its a debt free counter.Company paid dividend of 2.75rs for the fiscal.Management has hiked their stake from 25% odd to 53% in the last few years.

6)Fluidomat has increased the prices of its fluid couplings from 70000rs in fy06 to over 100000rs in fy13-14.It generated 5crs FCF last fiscal,toppled that with a return on equity of 30%+.This is one heck of a monopoly company.When you get a company which can increase the prices of its products without loosing its market share and then you talk about 30% ROE,You are really on something.

7)In case the economy starts recovering which it should as now the BJP guys are at the helms.Fluidomat can do a turnover of Rs50 Cr in two years.If it receives incremental order from Petronas.Turnover could increase to Rs100 Cr in 2 years.If the economy does not recover it can sustain its turnover at 30-35 Cr based on replacement demand and through its spare parts sales.Spare parts contribute nearly 40-45% of its revenues.

Latest update/My latest interaction with the management:As per the words of Pramod jain,"Getting an order is bit difficult because of our size and inexperience.For one ntpc tender we bidded for 22 lakhs vs voith's 2.7crs,yet the order went to voith.But we are hopeful of bagging future NTPC orders.As we grow, more orders will flow to the company".At the present capacity they can achieve a turnover of 65-70 crores.There are several developments going on but any of them could be a big one.A single order can change the fortunes of the company big time.Product is very crucial and its significance can be seen by this example-one company which had never used couplings - ordered fluidomat couplings for the first time.Fluidomat was expecting payback to be around 4-5 years but it happened before end of first year.Competition is tough with voith but they are gradually taking over businesses of others like elecon.Elecon used to outsource its requirement to fluidomat then it started copying fluidomat products and began supplying but last year they saw some rejections.

Consistency:Revenues in the last 11 years(2003-04 to 2013-14) increased from 5crs to 27crs.PAT has jumped from a mere 12 lakh to 5.7crs.

Conclusion:The promoters have no business interests except Fluidomat.No inter dealings and thus strong influence on the owned listed company.Company is getting lot of enquiries from both the domestic as well as the international markets.A single big order(there are talks of a 50crs order from Petronas) can change the fortunes of the company as mentioned earlier.The company is expected to grow 25-30% on bottomline for the coming couple of years.Revenues are bit difficult to predict as of now.Assuming it grows with a 30% CAGR in bottomline,the company would come end fy15-16 with PAT of 9.6crs.Thats 19 odd rs EPS for you.So assigning a PE multiple of 10x for fy16,I arrive at the target price of 195rs. Company is an amazing long term buy.

btw:I have recommended Fluidomat earlier at 68rs.But the story is too good and the scrip deserves much bigger levels than what its quoting at present.

Subscribe to:

Comments (Atom)